Dharma Markets Report #8: The Importance of Smart Contract Insurance in #DeFi

Your go-to resource for staying up to date with the decentralized financial system

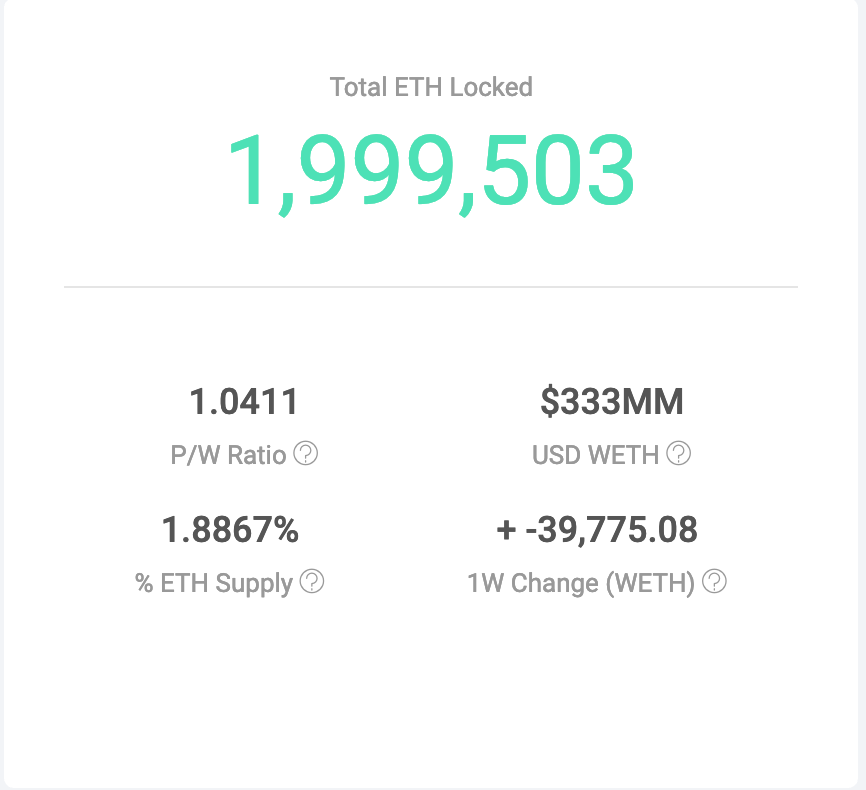

There’s little question that smart contracts are beginning to eat financial services — the numbers say it all. Not even a year into the “DeFi” movement and we already have over half a billion dollars locked up in financial smart contracts, a good chunk of which is coming from a new suite of decentralized lending platforms.

While it’s clear that value wants to be transcribed, stored, and transferred via smart contracts, many of the users we speak to, particularly those outside of the cryptocurrency ecosystem, are naturally apprehensive when it comes to moving their wealth on-chain.

Common questions we get include:

What happens if you’re hacked?

How do I know that your auditors found everything?

But Binance got hacked, can’t that happen to Dharma?

Smart contracts are a new paradigm that’s 10x, if not 100x, more superior t their analog counterparts. They’re more transparent, open, and are actually much more difficult to hack than a traditional bank. But technology alone won’t be enough to win new customers, and even if smart contracts are theoretically immune to hacks, we’ve already seen numerous failures in their short history.

At Dharma, we think insurance for smart contract-based financial services is one of the largest market opportunities in #DeFi today. Users need a way to ensure that the money they use within #DeFi won’t be hacked, stolen, or subject to technical failures.

The interesting part is that these insurance contracts don’t even need to live on-chain, they can be built using traditional practices so that newcomers enjoy the technological benefits offered by smart contracts, but with the same protection they enjoy in the real world.

It’s pretty obvious that insurance is an integral part of any financial system, but how might we build these contracts for DeFi?

The risks associated with smart contracts are very different than those inherent in traditional finance. This will invariably require a digital first approach. It means we’ll have to create new risk inputs like total lines of code, contract complexity, and how much value a smart contract has handled throughout its history.

All of these new factors can live inside today’s legal system or in the new brave world of on-chain finance. Qualified custodians have already begun bridging the traditional world into crypto by working with insurance brokers to create custom policies for their offerings. This should help institutional clients feel more comfortable onboarding into a new, digital financial system. On-chain smart contract insurance is also in the works. Nexus Mutual recently launched their communal risk-sharing DAO on the Ethereum mainnet and prediction market platforms like Augur can be used to create synthetic insurance contracts on certain events.

We’re extremely excited to watch the smart contract insurance space heat up. The more protection we can offer our users, the more liquidity, faith, and trust can be transferred into DeFi, which means more open, transparent, and programmable financial services for all.

DeFi Reads

Ask the Chain: It’s Bitcoin Springtime

Felipe Santa Ana of Paradigma Capital and Renato Shirakashi put out an excellent report digging into Bitcoin’s demand side. According to their findings, on-chain analysis supports the conclusion that Bitcoin, and the crypto markets more broadly, bottomed out in December. They specifically point to a number of new indicators, including MVRV and SOPR, that signify the market reached oversold levels on Bitcoin’s fall to $3,100 USD. The report also claims that we’ve transitioned into crypto spring — a time period marked by recovering prices and greater on-chain activity.

Kyle Samani of Multicoin Capital put out an excellent piece detailing the growing trend of developers building on top of chains other than Ethereum that better support the needs of more specific use cases. Kyle makes the case that Ethereum is best suited for open finance, and that the continued focus on financial applications has enabled ETH to develop a monetary premium. The post lays out the case for why developers building non financial uses cases will continue moving to other chains like Tron, EOS, and Kadena.

Decentralized Lending: An Overview

Antonio Juliano from dy/dx wrote an excellent overview covering the most popular decentralized lending platforms built on Ethereum. Antonio describes how users borrow and lend, what the most popular borrowing use cases are today, and how each platform optimizes for certain features. We highly recommend this piece for anyone wanting a detailed deep dive into the on-chain lending ecosystem.

The DeFi Series — A closer look into user community

Alethio released a data driven look into a number of decentralized finance platforms, specifically around the number of users that interact with the various products. From a thirty foot view, there have been ~39k unique #DeFi interactions made by ~11k unique users. The highest overlap between platforms is Maker and Compound, which share 1,302 unique users, likely because they offer such similar functionality. The post is filled with a ton of other insights, we highly recommend checking it out.

Crypto lending: too good to be true?

Roy from Wave Financial put out an excellent blog post on the state of crypto lending and specifically dug into whether or not today’s high lending rates have the legs to survive. Roy notes that today’s high rates are a result of speculation being the primary use cases for crypto borrowers. Viewed through this lens, it’s likely that rates remain high given the fact that speculators have the most demand for over-collateralized loans, not so much retail investors. Regardless of who’s borrowing, it’s still amazing to see smart contracts democratize access to the supply side of margin loans.

DeFi Data

The Death (and Revival?) of CDP 3228

The infamous CDP 3228 recently moved a majority of his CDP debt over to a decentralized lending platform that shall not be named (insert emoji). This is a result of numerous ‘ReFi with DeFi’ campaigns aimed at allowing CDP holders to refinance their Dai debt at a lower interest rate. What’s interesting is that CDP 3228 quickly re-opened his position shortly after ending his infamous reign, indicating to the broader market that he’s not finished accumulating ETH.

45m USD of loan originations in May

A recent announcement from Bloqboard highlighted the fact that over $45 million USD worth of loans were originated across DeFi platforms in May. This number has been steadily rising as the Maker risk team has restricted increased supply measures, showing that users are taking towards many of the new decentralized lending options available today.

DopeFi Links

JPMorgan Adds Privacy Features to Ethereum-Based Quorum Blockchain

Big news for the Ethereum community last week as JPMorgan built an extension to the Zether Protocol, a system that provides privacy features for account based blockchains. The firm plans to open source their code shortly, which will enable much more experimentation of ZKP’s on Ethereum.

Grayscale Gets Approval for Retail Ethereum Trust

Grayscale made headlines for getting FINRA approval to list an Ethereum Investment Trust similar to their GBTC investment vehicle. The new trust, ETHE, will give a new set of investors the ability to have ETH exposure in their portfolio. This news came on the heels of Grayscale’s recent ‘Drop Gold’ marketing campaign.

Dai was finally listed on Coinbase!

This is a big moment for the decentralized finance ecosystem as users can easily get their hands on Dai. Coinbase now supports Dai trading against USD, USDC, and ETH, bringing some much needed liquidity to the asset.

Vishesh recently put together a new website called Dai Decipher that provides a 24 hour volume-weighted-average-price for Dai. This is a great tool for seeing how Dai is trading across various exchanges. We’re excited to see Vishesh’s tool be used more frequently in Maker governance discussions.

Announcements

We recently added support for USDC. Now, users of Dharma can borrow and lend USDC at 8% APR from anywhere in the world, instantly.

If you have any comments or suggestions regarding the product, like assets you’d like to see added or loan terms you’d like supported, feel free to email max [at] dharma [dot] io.