Dharma Markets Report #7: Interest Rate Indexes in Crypto

Your go-to resource for staying up to date with the decentralized financial system

With overcollateralized lending quickly becoming the “hello world” of programmable money, a large number of firms have created products to help service the crypto market’s pent up demand for credit. And while originations are skyrocketing, the market remains inefficient and fractured today.

A big problem in particular is a lack of agreed upon reference rates. Without a set of standard rates for the market to coalesce around, it’s extremely difficult for participants to accurately price risk and the opportunity cost of their assets. What this results in is decreased participation and lower liquidity.

In traditional finance, capital markets rely on two indexes, LIBOR and the federal funds rate, to provide a reference point for the cost of capital. Nearly all financial institutions peg their operations to these two indexes, making it much easier for them to transact with one another as everyone can come to a consensus on an accurate market rate. These rates also permeate all types of consumer loans like credit cards, home, and auto as banks adjust their offerings based on the rates that they’re charged.

Just like the legacy system has been able to coordinate around shared standards, the crypto capital markets will need to establish interest rate indexes to help bolster liquidity and price discovery. This undertaking won’t be easy, particularly because of the various inputs that go into each type of agreement. For example, the fixed-term Dai loan we offer at Dharma is much different than the open ended term loan an investor gets through Compound. As such, unique indexes will have to be created for all of the various lending agreements offered in the crypto markets.

Luckily, two firms have begun building interest rate indexes for the crypto lending markets.

The Block’s DIPOR

Originally introduced by The Block, the Decentralized Inter-Protocol Offered Rate (DIPOR) is an interest rate index specifically created for #DeFi lending platforms. DIPOR attempts to provide a volume weighted average interest rate for borrowing various cryptocurrencies within DeFi as well as a tool for Maker’s risk team to use when conducting stability fee research.

If implemented today, DIPOR would help MKR holders more accurately adjust the stability fee to help keep Dai closer to its $1.00 USD peg. As Matteo points out, when Dai trades under a dollar, Maker wants to guide prospective borrowers to borrow from alternate platforms like Dharma to avoid minting new Dai. To incentivize this behavior, MKR holders would raise the stability fee above the DIPOR rate. On the other hand, if Dai trades above the dollar, MKR holders would lower the stability fee below DIPOR to incentivize more CDP creation and subsequent Dai minting.

A big benefit of having an interest rate index that lives squarely within the decentralized finance realm is that all of the underlying data is transparent and auditable on-chain. With DeFi, scandals like the one that took down LIBOR in 2012 are impossible because there’s no centralized party in charge of reporting interest rates.

A prototype of Dai DIPOR is already live on LoanScan — it provides a rolling 24 hr volume weight average borrow rate based on Compound and MakerDAO.

Messari’s CIRI

While DeFi is a rapidly growing part of the crypto capital markets, Bitcoin lending markets are much larger and have existed for quite a while longer.

In an effort to standardize Bitcoin borrowing rates, Messari recently released the Crypto Interest Rate Index (CIRI), a short-term risk-free rate for Bitcoin.

Their index is comprised of the following instruments:

BitMex futures implied rate

CME futures implied rate

Bitfinex lending rate

Poloniex lending rate

There are a few reasons these specific rates were included. For one, to have a risk-free rate, the borrower needs to be fully collateralized. In a space as nascent as crypto, counterparties aren’t as well funded as, let’s say, the US government, so these agreements aren’t included in the CIRI. Another important aspect of the methodology is that they only use instruments that mature within 90 days. That’s because there’s only a small number of instruments that allow for loans longer than 90 days, which would skew the value of the CIRI.

Messari did note that this index will heavily rely on centralized lending avenues reporting the rates on a frequent basis. As it stands today, the rates reported in the CIRI vay widely, and would definitely benefit from the likes of Genesis, BlockFi, and Unchained reporting their daily rates.

DeFi Reads

The DeFi Series — An Overview of the ecosystem and major protocols

Alethio, an Ethereum data company, wrote an in-depth analysis covering various #DeFi protocols as well as the user overlap between Maker and Compound. The piece provides great summaries on MakerDAO and the Dai credit system, as well as Compound, Uniswap, and Augur. Alethio then goes on to highlight the total number of unique borrowers and suppliers of Compound as well as CDP openers. Interestingly enough, Alethio found that there 9,539 unique addresses that used both Compound and MakerDAO. We’re curious to know what that number looks like if you throw Dharma in the mix.

Multicoin Capital released a big website overhaul and highlighted their primary crypto theses. They specifically mention open finance as one of the most investable use cases in the space, saying that this new breed of financial infrastructure will become more accessible and efficient than today’s existing rails. Multicoin also makes the point that open finance will first win retail markets before on-boarding institutions.

Bitcoin Can’t Fix Venezuela: I Should Know

Diana Aguilar wrote an excellent piece that debunks many of the myths the crypto community has previously made about the effect Bitcoin, and cryptocurrencies more broadly, have had in Venezuela. Diana notes that while Bitcoin does provide a glimmer of hope, Venezuela’s infrastructural gaps prevent it from being a place where cryptocurrency can be adopted by everyone. But while many of today’s claims are overstated, Diana does attest to the benefits Bitcoin brings to use cases like remittances and payroll for independent contractors.

The Covalent team put together an interesting analysis on Uniswap’s traction using on-chain metrics. This piece provides valuable insights into the top exchanges created, average transaction sizes, user retention rate, etc.

DeFi Data

CDP Refinancing

Since we launched support for borrowing and lending Dai, our growth has been staggering. In particular, we’ve seen a number of the largest CDP holders move their Dai debt over to Dharma. After we launched our #ReFi with #DeFi campaign, we had an influx of borrow demand from users wanting to lock in a fixed term rate amidst an increasing stability fee. In the span of just two weeks, Dharma originated over $6 million USD in Dai loans and we now have over $16 million USD worth of collateral locked in our smart contracts.

Dai’s Return

Dai’s peg seems to be what everyone in DeFi talks about these days. Soon after Dai began trading between $0.95 - $0.97, MKR holders quickly raised the stability fee all the way up to 19.5% APR. The interest rate increase, along with some healthy buying demand created by secondary Dai markets, has helped bring Dai closer to its $1.00 USD peg. It will likely take some time until market makers are able to unload enough inventory, but all signs point to a healthy market responding to supply and demand.

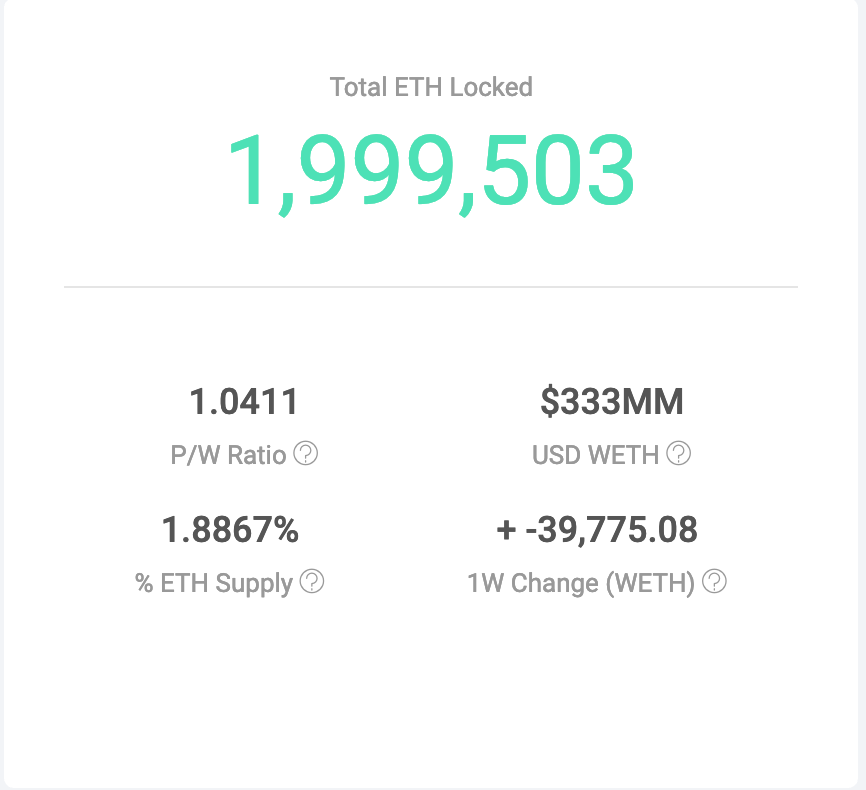

ETH Locked in MakerDAO Below 2 million

As a reaction to the recent stability fee hikes, the total number of ETH locked in MakerDAo fell below the coveted 2m ETH mark. CDP holders have been closing out their positions in an effort to avoid increased interest payments.

#Dopefi Links

Grayscale to Investors: Drop Gold

Grayscale launched their provocative ad campaign last week urging gold investors to consider investing in a digital alternative. The advertisement aired across a number of major news networks and has made its rounds amongst most financial circles. Grayscale’s campaign arrived on the heels of a number of product launches geared towards making it easier for institutions to get exposure to the asset class.

Regulators Ready to Approve Ethereum Futures

A member of the CFTC commented that the firm is interested in launching an Ether futures product similar to the BTC futures product they rolled out at the end of 2017. Ether futures would help institutions familiarize themselves with the asset as well as bring some much needed liquidity to the markets. Assuming a successful futures launch, ETH borrowing should see an uptick as market makers and basis traders gear up to trade the product.

Fidelity on Institutional Investors

Fidelity investments showcased their new research in regards to institutional appetite for digital assets. Their report found that institutional investors are overwhelmingly positive about digital assets, with 47% of surveyed investors believing it was an innovative technology play. Among the investors surveyed, 22% already had exposure to the asset class, with another 47% saying digital assets belong in their portfolios. It will be interesting to see how institutional investors decide to engage with DeFi tools once they’re on boarded into the ecosystem.

Ethereum.org got a much needed redesign as the community attempts to re-focus its efforts on a number of key use cases including programmable money. The new site makes it easy for newcomers to learn about, use, and build on Ethereum.